The recent Fed rate cut has sent ripples across the financial landscape, affecting everything from consumer debt to mortgage rates. As the Federal Reserve lowers the cost of borrowing, experts predict a beneficial impact for individuals grappling with credit card debt and potential homebuyers. This pivotal decision, marking the Fed’s first reduction in four years, aims to stimulate economic growth while also addressing concerns regarding inflation. With the Fed’s proactive stance, many are looking to see how this will alleviate financial pressures for consumers in the coming months. As interest rates adjust in response to this change, understanding the nuances of these developments will be crucial for anyone seeking to navigate the current economic climate.

The recent decision by the central bank to lower interest rates is a significant move that many experts believe will promote financial easing. By reducing the cost of borrowing, this monetary policy shift aims to foster a favorable environment for consumers and businesses alike. With implications that stretch from mortgage affordability to the management of personal loans, the cut in rates is designed not only to assist individuals but also to spur broader economic activity. Observations from market analysts suggest that as this financial strategy unfolds, it will be vital for consumers to stay attuned to how their financial commitments might be influenced by these changing interest dynamics. Ultimately, this pivotal action comes at a critical juncture, poised to inject optimism into the economy.

Understanding the Recent Fed Rate Cut

The Federal Reserve’s recent decision to cut the key interest rate by half a percentage point marks a significant shift in their monetary policy. This move, which is the first rate cut in four years, is primarily aimed at lowering borrowing costs for consumers and businesses alike. By doing so, the Fed hopes to stimulate economic growth, especially in sectors that heavily depend on credit, such as housing and consumer loans. The instinct behind this policy change is to combat potential economic slowdown and support job growth while managing inflation rates.

Economist Jason Furman highlights that with the reduction in federal rates comes a likely decrease in mortgage rates, making homebuying more accessible for many consumers. This is particularly vital in a high-cost housing market where affordability has become a pressing concern. Moreover, the Fed’s flexibility to adjust rates based on labor market changes instills a sense of confidence in borrowers, encouraging more spending, investing, and lending activity in the economy.

Frequently Asked Questions

What is a Fed rate cut and how does it affect interest rates?

A Fed rate cut refers to the Federal Reserve lowering the federal funds rate, which is the interest rate at which banks lend to each other. This decrease leads to lower interest rates across the economy, making borrowing cheaper for consumers and businesses. As a result, consumers may see a reduction in mortgage rates, credit card rates, and car loan rates, encouraging economic growth and consumer spending.

How does a Fed rate cut influence mortgage rates?

A Fed rate cut typically leads to lower mortgage rates, as lenders adjust their interest rates in response to the cheaper cost of borrowing. This is beneficial for homebuyers and can help alleviate the housing affordability crisis by making mortgage payments more manageable for prospective homeowners.

Can the Fed rate cut provide consumer debt relief?

Yes, a Fed rate cut can provide consumer debt relief by decreasing interest rates on various types of loans, including credit cards and auto loans. As the cost of borrowing decreases, consumers may find it easier to pay down existing debt or take on new loans under more favorable terms.

What might be the economic impact of multiple Fed rate cuts over time?

Multiple Fed rate cuts can stimulate economic growth by encouraging borrowing and spending. This can lead to higher consumer confidence, job creation, and increased investment from businesses. However, sustained low rates may also risk higher inflation in the long term.

Why did the Federal Reserve decide to cut interest rates now?

The Federal Reserve decided to cut interest rates to address potential economic slowdowns and to provide support for consumers and businesses. By lowering rates, the Fed aims to stimulate borrowing, promote economic activity, and balance the risk of recession while ensuring stable employment levels.

How often does the Federal Reserve make decisions about interest rates?

The Federal Reserve meets regularly, typically eight times a year, to discuss and make decisions regarding interest rates. At these meetings, the Federal Open Market Committee evaluates economic conditions and may adjust the federal funds rate to achieve its monetary policy goals.

What can consumers expect regarding interest rates after the recent Fed rate cut?

Consumers can expect interest rates on various loans to potentially decrease further as the Federal Reserve eases its monetary policy. However, they should remain cautious, as uncertainty in economic conditions can affect how quickly and significantly rates may fall.

How does the Fed’s rate policy affect stock market investors?

The Fed’s rate policy has a significant impact on stock market investors. Generally, lower interest rates lead to higher stock prices as borrowing costs decrease, consumer spending increases, and companies may invest more, boosting overall corporate profit margins.

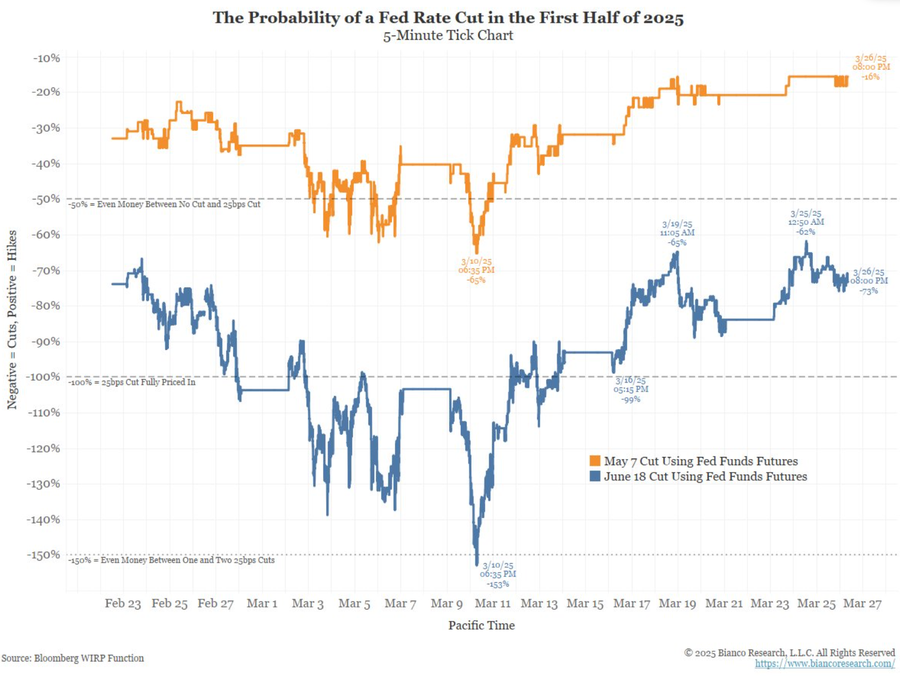

Will there be further Fed rate cuts before the year ends?

There is strong speculation about further Fed rate cuts before the year ends, with forecasts suggesting two additional 25 basis point cuts. However, any future cuts will depend on economic indicators such as inflation and employment rates.

What are the risks of continuing to lower the Fed rate?

Continuing to lower the Fed rate carries risks, such as potentially creating asset bubbles in markets or leading to higher inflation if the economy overheats. The Fed must carefully monitor economic indicators to balance the benefits of stimulating growth with the risks associated with low interest rates.

| Key Point | Details |

|---|---|

| First Fed Rate Cut in Four Years | The Federal Reserve cut interest rates by half a percentage point to lower borrowing costs. |

| Positive Impacts | Benefits for consumers with debt, homebuyers, and investors in the stock market. |

| Continued Easing Possible | Fed Chairman Powell hinted at more cuts potentially totaling another half point by year end. |

| Fed’s Risk Management | The Fed aims to balance slowing growth to combat inflation without leading to unemployment. |

| Impact on Economic Growth | Rate cuts may lead to job creation and slight increases in economic growth over time. |

| Mortgage Rates and Housing | Mortgage rates are likely to decrease further, which will aid housing affordability. |

| Consumer Debt Relief Expectations | Consumers may take longer to feel the impact of the Fed rate cuts on interest rates. |

Summary

The recent Fed rate cut marks a significant moment in economic policy, providing consumers with potential relief from borrowing costs. As the Federal Reserve lowers interest rates, the anticipated benefits include lower mortgage rates and relief for those carrying credit card debt. However, the timeline for these benefits remains uncertain, as it is heavily influenced by other economic factors and market expectations. The Fed’s commitment to adjusting rates responsibly suggests a pathway to support both Wall Street and Main Street as we navigate this critical juncture in economic recovery.