The 2017 Tax Cuts and Jobs Act (TCJA) marked a significant turning point in U.S. tax policy, with sweeping changes aimed at stimulating economic growth and international competitiveness. By slashing corporate tax rates from 35% to 21%, the legislation aimed to boost business investments while introducing expanded provisions like the Child Tax Credit to support families. However, as Congress now prepares for potential tax battles in 2025, key provisions of the TCJA—including those affecting corporate tax revenue and individual taxpayers—are set to expire, leading to debates that echo Chodorow-Reich’s recent tax reform analysis. Critics question whether the expected growth in corporate profits and investment materialized, while proponents argue that these cuts could pay for themselves over time. As the effects of the TCJA are scrutinized, the potential implications for both corporate tax rates and personal tax benefits loom large in upcoming elections.

The Tax Cuts and Jobs Act of 2017, often categorized as a transformative legislative overhaul, reshaped the landscape of taxation in America. This law significantly reduced the financial obligations of corporations, aiming to enhance competitiveness and drive job creation in a rapidly evolving economy. At the same time, it expanded tax benefits for families through measures like the enhanced Child Tax Credit, a move intended to alleviate economic pressure on households. As the U.S. government grapples with the implications of these changes, the discourse around fiscal strategy, corporate tax revenue, and the broader socio-economic impact continues to be a hotly debated topic. Understanding the nuances of these tax reforms will be crucial for voters as they prepare to engage in the electoral discussions surrounding fiscal policy.

Understanding the 2017 Tax Cuts and Jobs Act

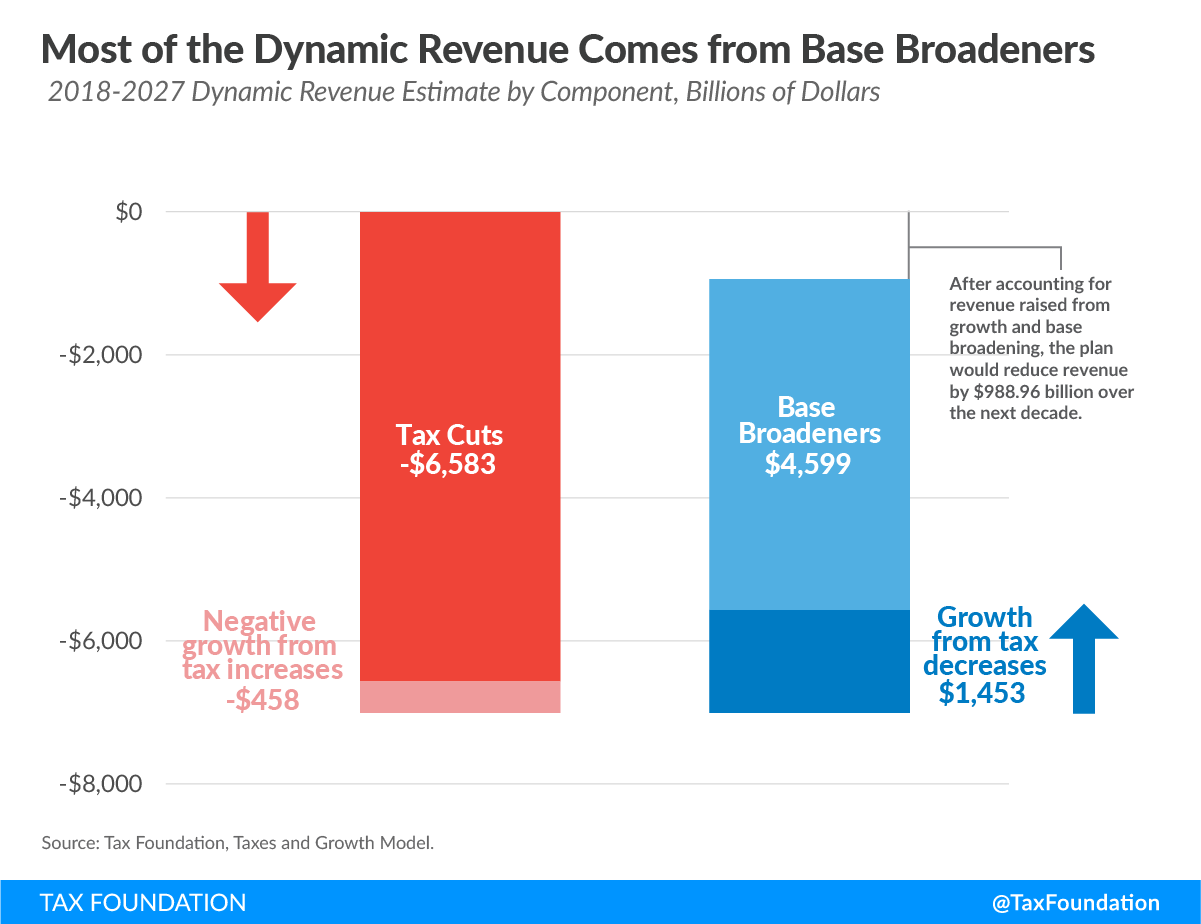

The 2017 Tax Cuts and Jobs Act (TCJA) marked a significant shift in U.S. tax policy, reducing the corporate tax rate from 35% to 21%. This legislative change was primarily aimed at reinvigorating business investment and spurring economic growth. However, the implications of these cuts have been the subject of intense scrutiny, particularly concerning their impact on corporate tax revenue and wage growth. Harvard economist Gabriel Chodorow-Reich, along with his colleagues, has conducted an extensive analysis of this law, highlighting the complexities and nuances of its effects on the economy.

While the intent behind the TCJA was to stimulate the economy by lowering corporate taxes, results have varied. Chodorow-Reich’s research indicates that while there were modest increases in wages and corporate investments, these growth metrics did not adequately offset the massive drop in corporate tax revenue, estimated at $100 billion to $150 billion annually. This raises important questions about the efficacy of tax cuts as a tool for economic stimulation, suggesting that policymakers may need to reevaluate the strategy they employ for tax reform, especially in light of upcoming fiscal challenges as key provisions of the TCJA are set to expire.

Frequently Asked Questions

What are the main effects of the 2017 Tax Cuts and Jobs Act on corporate tax rates?

The 2017 Tax Cuts and Jobs Act (TCJA) significantly reduced the corporate tax rate from 35% to 21%, aimed at making the U.S. more competitive globally. This change was intended to spur business investments and increase corporate tax revenue; however, studies, including one by Gabriel Chodorow-Reich, indicate that while there were modest increases in investments, corporate tax revenue initially plummeted by 40%.

How did the 2017 Tax Cuts and Jobs Act impact the Child Tax Credit?

The 2017 Tax Cuts and Jobs Act expanded the Child Tax Credit to provide more financial support for families, an important provision especially for low- and middle-income households. However, this expansion is set to expire in 2025, which is causing growing concern among voters as they brace for upcoming tax debates.

What was the conclusion of Gabriel Chodorow-Reich’s analysis of the 2017 Tax Cuts and Jobs Act?

Gabriel Chodorow-Reich, in his economic analysis of the 2017 Tax Cuts and Jobs Act, found that while there were increases in business investments, the overall tax cuts did not generate sufficient corporate tax revenue to offset the losses. The analysis suggested that the most effective way to stimulate further investment would be through restoring expensing provisions rather than solely relying on reduced tax rates.

Did the 2017 Tax Cuts and Jobs Act successfully promote business investment?

The 2017 Tax Cuts and Jobs Act did lead to a reported 11% increase in capital investments, primarily driven by provisions allowing immediate expensing of new investments. However, the effectiveness in promoting broader business growth and wage increases remains debated, as the actual wage growth was lower than anticipated.

What critiques have emerged regarding the corporate tax revenue following the 2017 Tax Cuts and Jobs Act?

Post-implementation of the 2017 Tax Cuts and Jobs Act, corporate tax revenue saw a substantial drop of 40%, raising critiques about the long-term viability of such tax reductions. Despite a rebound in corporate profits observed in subsequent years, experts like Gabriel Chodorow-Reich advocate for a nuanced discussion regarding the interplay between tax rates and corporate behavior.

How does the expiration of the 2017 Tax Cuts and Jobs Act provisions affect taxpayers?

As key provisions of the 2017 Tax Cuts and Jobs Act approach expiration at the end of 2025, taxpayers may face changes in tax benefits, particularly the Child Tax Credit. Renewing or altering these provisions may lead to significant impacts on individual tax obligations and overall financial stability for families.

What proposals are being considered in relation to the 2017 Tax Cuts and Jobs Act as it nears expiration?

As the provisions of the 2017 Tax Cuts and Jobs Act near expiration, proposals have surfaced from both parties. Some, like Kamala Harris, advocate for increasing corporate tax rates to fund other initiatives while others, including Donald Trump, support further reductions to stimulate growth. The upcoming debates will likely focus heavily on balancing revenue generation against potential economic growth.

| Key Points |

|---|

| The 2017 Tax Cuts and Jobs Act (TCJA) aimed to reduce corporate tax rates from 35% to 21%. It was designed to stimulate investment and economic growth. |

| Key provisions of the TCJA included immediate expensing for capital investments and research expenditures. |

| The law faced criticism for lowering tax revenues significantly, estimated at $100 to $150 billion annually. |

| Recent analysis indicates modest increases in wages and investments, although benefits were less than expected. |

| Debates continue regarding whether to cut or raise corporate tax rates, especially with upcoming expirations of provisions. |

| Corporate tax revenue declined initially by 40% after the TCJA was enacted, but rebounded starting in 2020. |

Summary

The 2017 Tax Cuts and Jobs Act represents a significant shift in U.S. tax policy aiming to lower corporate tax rates and incentivize business investment. Despite initial hopes for substantial economic growth and increased wages, analysis reveals that overall gains were modest and tax revenue drastically declined initially. As key provisions are set to expire, the upcoming debate surrounding the renewal or modification of the TCJA will undoubtedly shape future economic strategies and political campaigns.