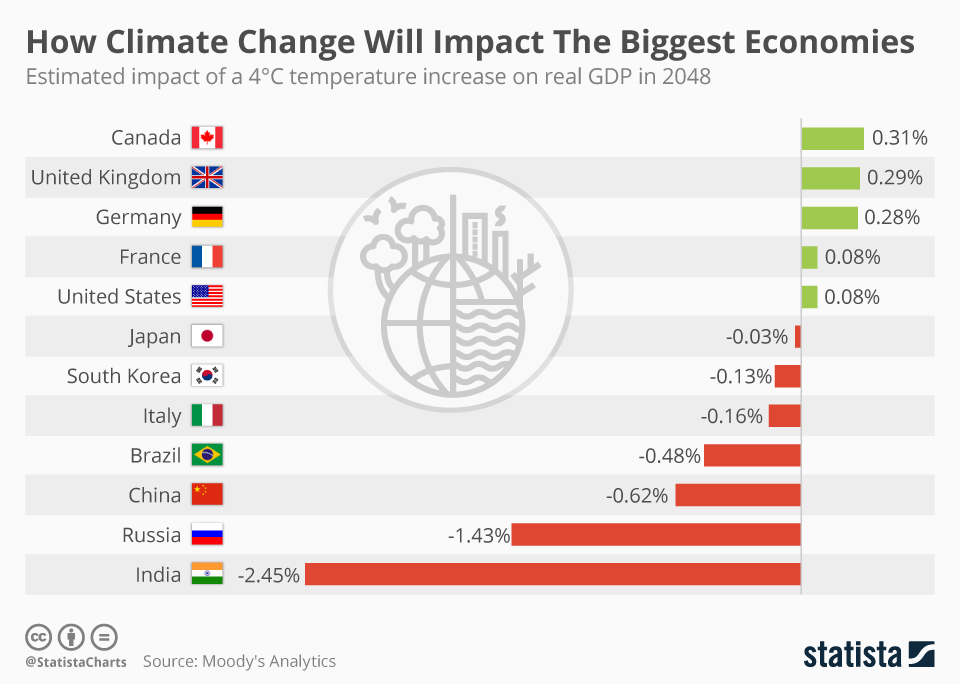

The economic impact of climate change is becoming increasingly dire, as new studies reveal that the costs associated with rising global temperatures may be six times greater than previous estimates. Climate change economics has shown a worrying disconnect between environmental data and macroeconomic forecasts, often downplaying how significantly GDP and climate impact are intertwined. As global temperatures increase, the world risks suffering substantial reductions in productivity, with some projections indicating an alarming 12 percent decline in global GDP for each additional degree Celsius. This emerging data underscores the urgent need for effective decarbonization policies to mitigate the escalating costs of climate change, which are no longer just environmental concerns but critical economic challenges. With the potential for devastating impacts on societal wealth and economic viability, addressing the cost of climate change is more urgent than ever.

As the planet experiences unprecedented shifts in climate patterns, the repercussions are seeping into the very fabric of our global economy. The fiscal consequences borne from climate change are now a pressing concern that intertwines with discussions on climate change economics, necessitating a reevaluation of traditional economic models. The looming threat of GDP loss, driven by rising global temperatures, fuels the necessity for robust decarbonization strategies. These strategies must not only prioritize environmental sustainability but also safeguard economic prosperity against the backdrop of extreme weather events. Such comprehensive approaches will ensure that future generations inherit a planet capable of supporting both ecological health and economic stability.

The Economic Consequences of Rising Global Temperatures

The economic consequences of rising global temperatures have become increasingly apparent as new studies reveal alarming estimates of the impact on global GDP. According to recent research, every additional degree Celsius increase in global temperature is projected to decrease global productivity by a staggering 12 percent. This threatens not only the economic output but also the livelihoods of millions, particularly in vulnerable regions. With the world already experiencing a temperature rise of 1°C since the pre-industrial era, the urgency to address climate change through effective economic policies becomes imperative.

These economic projections indicate a much larger cost of climate change than previously anticipated. The predictions assert that the economic toll will peak approximately six years after each individual temperature rise, highlighting the long-term ramifications of climate change. This new economic understanding necessitates a shift in how macroeconomists approach climate-related issues, integrating insights from both environmental science and economic modeling to formulate a clearer picture of the future. In doing so, economists can better inform public policy and foster strategies that mitigate these adverse economic impacts.

Rethinking Climate Change Economics

For years, climate change economics focused on localized temperature variations while overlooking the broader implications of global temperature increases. Researchers now advocate for a new framework that considers the cumulative impacts of global warming on economic productivity. This innovative approach reveals that extreme weather events—exacerbated by rising temperatures—have dire consequences for both capital and workforce productivity, substantially undermining long-term economic gains. The disconnect between traditional economic forecasts and climate science has prompted scholars to reevaluate their methodologies for assessing the cost of climate change.

By applying new models that connect global temperature increases to economic indicators, economists shed light on the broader ramifications of climate change. The findings suggest that the social cost of carbon should reflect these findings, leading to more robust decarbonization policies. This evolution in climate change economics emphasizes the necessity of integrating environmental data into economic assessments to achieve effective and sustainable solutions for climate-related issues.

The Cost of Climate Change and Economic Growth

The intersection of climate change and economic growth raises critical questions about sustainability in a warming world. Recent studies highlight that while economic growth may continue, the trajectory of such growth is severely hindered by climate impacts. For instance, should global temperatures rise another 2°C by the end of the century, economic output could face declines of up to 50%, a magnitude comparable to the Great Depression but persisting indefinitely. This chilling forecast underscores the importance of proactive decarbonization strategies to mitigate future losses.

Furthermore, the analysis of the costs associated with climate change takes on fresh significance as policymakers seek to balance economic priorities with environmental preservation. Utilizing updated estimations of the social cost of carbon can influence how investments and policies are structured. These insights suggest that failing to address climate change could ultimately compromise the economic stability that nations aim to achieve, making a compelling case for immediate and coordinated action in the areas of climate policy and economic reform.

Decarbonization Policy: Economic Necessity or Environmental Idealism?

Decarbonization strategies are often perceived as a luxury, but recent findings position them as an economic necessity. With the social cost of carbon projected at $1,056 per ton, compared to outdated estimates of just $185, the case for robust decarbonization policies becomes undeniable. The Inflation Reduction Act, with costs estimated at $95 per ton, demonstrates the potential for economic growth while transitioning to a greener economy. This recalibration of the fiscal implications reveals that investing in decarbonization yields significant returns, supporting both economic resilience and environmental health.

As countries formulate their decarbonization policies, understanding the economic impact of climate change is crucial in aligning climate goals with sustainable economic development. The projections suggest that proactive investments in green technology and infrastructure not only mitigate climate risks but also create jobs and stimulate economic growth. Bridging the gap between economic growth and environmental responsibility is essential for crafting forward-thinking policies that ensure a sustainable future amid the challenges posed by climate change.

Global Temperature Increase and Its Economic Implications

The implications of a global temperature increase extend far beyond environmental concerns, severely impacting the economic landscape. Rising temperatures correlate with a surge in extreme weather events, which pose significant threats to capital, infrastructure, and overall productivity. As each additional degree raises economic costs, understanding these dynamics becomes crucial for governments and businesses alike. A holistic approach that links climate models with economic forecasts can enhance strategic planning and risk management practices, offering better preparedness for the adverse consequences of climate change.

Moreover, the focus on global temperature as a central economic variable offers new insights into the relationship between climate change and GDP performance. Research indicates that countries that fail to adequately address carbon emissions may face stark economic penalties, undermining their growth potential. By prioritizing temperature management and investing in sustainable practices, economies can not only avert disastrous losses but also pave the way for a more resilient economic framework that thrives in harmony with a changing climate.

The Connection Between Climate Change and Economic Stability

Climate change is increasingly recognized as a central threat to economic stability, presenting multifaceted risks that affect global markets and national economies. As severe weather patterns escalate and environmental conditions deteriorate, they threaten the fabric of economic systems through damage to infrastructure and property. Understanding these interconnections is vital for policymakers, who must create adaptive strategies that encompass both environmental sustainability and economic resilience in the face of a changing climate.

The potential for climate change to disrupt not only individual sectors but entire economies highlights the need for comprehensive approaches to economic planning. By integrating climate risk assessments into economic models, nations can foster a proactive stance that mitigates risks and enhances preparedness. Acknowledging these economic realities can drive innovation, pushing industries toward sustainable practices that ultimately contribute to greater economic stability and environmental stewardship.

Adapting Economic Policies for a Warming World

To confront the economic realities of climate change, adaptation in economic policies is paramount. Policymakers must adapt existing economic frameworks to consider the impending risks posed by climate fluctuations. This means reassessing traditional economic growth models and ensuring that climate change implications are woven into policy discussions from the onset. By employing forward-thinking approaches that prioritize sustainability, policymakers stand better positioned to cultivate resilience in their economies.

Adaptation strategies should incorporate diverse stakeholder perspectives, including environmental scientists and economists, for a more holistic policy framework. Comprehensive adaptation not only addresses the immediate economic threats but also positions countries favorably for long-term growth in a warming world. By doing so, nations can transition towards economies that are not only prepared for the changes ahead but are also pioneers in sustainable development practices globally.

The Role of Innovation in Limiting Climate Economic Damage

Innovation plays a crucial role in addressing the economic impacts of climate change and is essential for driving the transition towards sustainable practices. Technological advancements in energy efficiency, renewable resources, and carbon capture are key components in mitigating climate damage while simultaneously fostering economic growth. By investing in innovative solutions, economies can enhance productivity, create new job opportunities, and reduce their carbon footprint to combat the escalating threat of climate change.

The global shift towards a low-carbon economy hinges on the successful implementation of these innovative technologies. As such, governments and private sectors must collaborate to stimulate research and development in climate-focused innovations. This effort not only combats economic decline driven by climate change but also positions nations as leaders in the burgeoning green economy, creating a virtuous cycle that supports sustainable growth and environmental responsibility.

Understanding the Social Cost of Carbon

Understanding the social cost of carbon (SCC) is essential to framing climate policies that protect economic stability while mitigating climate change. The SCC provides a monetary estimate of the economic damages associated with the emission of one additional ton of carbon dioxide. With recent findings projecting the SCC at $1,056 per ton, policymakers are equipped with compelling evidence to justify stronger decarbonization initiatives. This reflection of true climate costs advocates for strategic investment in sustainability efforts that promise economic returns.

Moreover, the growing awareness of the economic relevance of the social cost of carbon serves as a vital component of rational policymaking. By explicitly incorporating SCC into climate accounting, governments can foster efforts that not only curb emissions but also underpin economic development. In acknowledging the true costs of inaction, nations can build a shared commitment to addressing climate challenges while simultaneously promoting economic growth.

Frequently Asked Questions

What is the economic impact of climate change on global GDP?

The economic impact of climate change on global GDP is projected to be significant, with estimates indicating that every additional 1°C rise in temperature could lead to a 12 percent decline in global GDP. This forecast is six times larger than previous estimates, indicating a severe threat to economic productivity caused by higher temperatures.

How do climate change economics factor into future economic growth predictions?

Climate change economics suggests that although economic growth may continue, the overall output will be severely affected by climate change. Projections indicate that if global temperatures rise by 2°C, it could reduce economic output and consumption by as much as 50%, implying that future economic growth may not offset the adverse effects of climate change.

What is the calculated social cost of climate change according to recent studies?

Recent studies calculate the social cost of climate change at approximately $1,056 per ton of carbon, significantly higher than earlier estimates of around $185 per ton. This updated figure reflects the increasing economic impact of carbon emissions and reinforces the need for effective decarbonization policies.

How does decarbonization policy relate to the cost of climate change?

Decarbonization policy is directly influenced by the economic impact of climate change, as effective implementation can reduce the high social costs associated with carbon emissions. Recent analysis shows that for economies like the U.S. and European Union, the cost-benefit analysis of decarbonization is favorable, providing economic incentives to reduce greenhouse gas emissions.

What are the implications of global temperature increase on economic productivity?

The implications of a global temperature increase on economic productivity are dire, as each 1°C rise is linked to a 12 percent drop in productivity. This link emphasizes the connection between climate change and its economic fallout, necessitating urgent action to mitigate rising temperatures and their harmful effects.

How does extreme weather relate to the economic impact of climate change?

Extreme weather events, exacerbated by climate change, contribute significantly to economic losses by affecting productivity and capital. The increased frequency of these events correlates with rising global temperatures, highlighting the need to factor extreme weather into economic impact assessments related to climate change.

What are the future economic scenarios if climate change continues unabated?

If climate change continues unabated, future economic scenarios suggest that the world’s GDP could suffer drastic declines, with estimates showing potential reductions in output of up to 50% by the end of the century with a 2°C increase in global temperatures. This bleak outlook underscores the pressing need for comprehensive climate action.

| Key Point | Description |

|---|---|

| Economic Impact Estimates | New forecasts indicate a 12% decline in global GDP for each additional 1°C rise in temperature, significantly larger than prior estimates. |

| Temperature and Economic Research | The study’s authors utilized global temperature data to analyze economic effects, revealing a correlation between rising temperatures and increased extreme weather events. |

| Long-term Projections | An anticipated 2°C rise in temperature by 2100 could reduce output by 50%, a loss comparable to the Great Depression. |

| Social Cost of Carbon | This new analysis places the social cost of carbon at $1,056/ton, significantly higher than previous local estimates, underscoring the economic argument for decarbonization policies. |

| Decarbonization Benefits | The findings suggest that decarbonization strategies offer substantial economic benefits, making them a worthwhile investment for economies such as the U.S. and EU. |

Summary

The economic impact of climate change is alarmingly significant, challenging previous estimates with projections indicating that every additional 1°C rise in temperature can cause a 12% decline in global GDP. Recent research underscores the urgent need for nations to adopt decarbonization measures, as the long-term economic implications of inaction could lead to immense losses, potentially diminishing our economic future. By recalibrating the social cost of carbon, the study reinforces the validity of investing in climate change mitigation strategies, confirming that the costs associated with addressing climate change are far outweighed by the economic benefits of proactive measures.