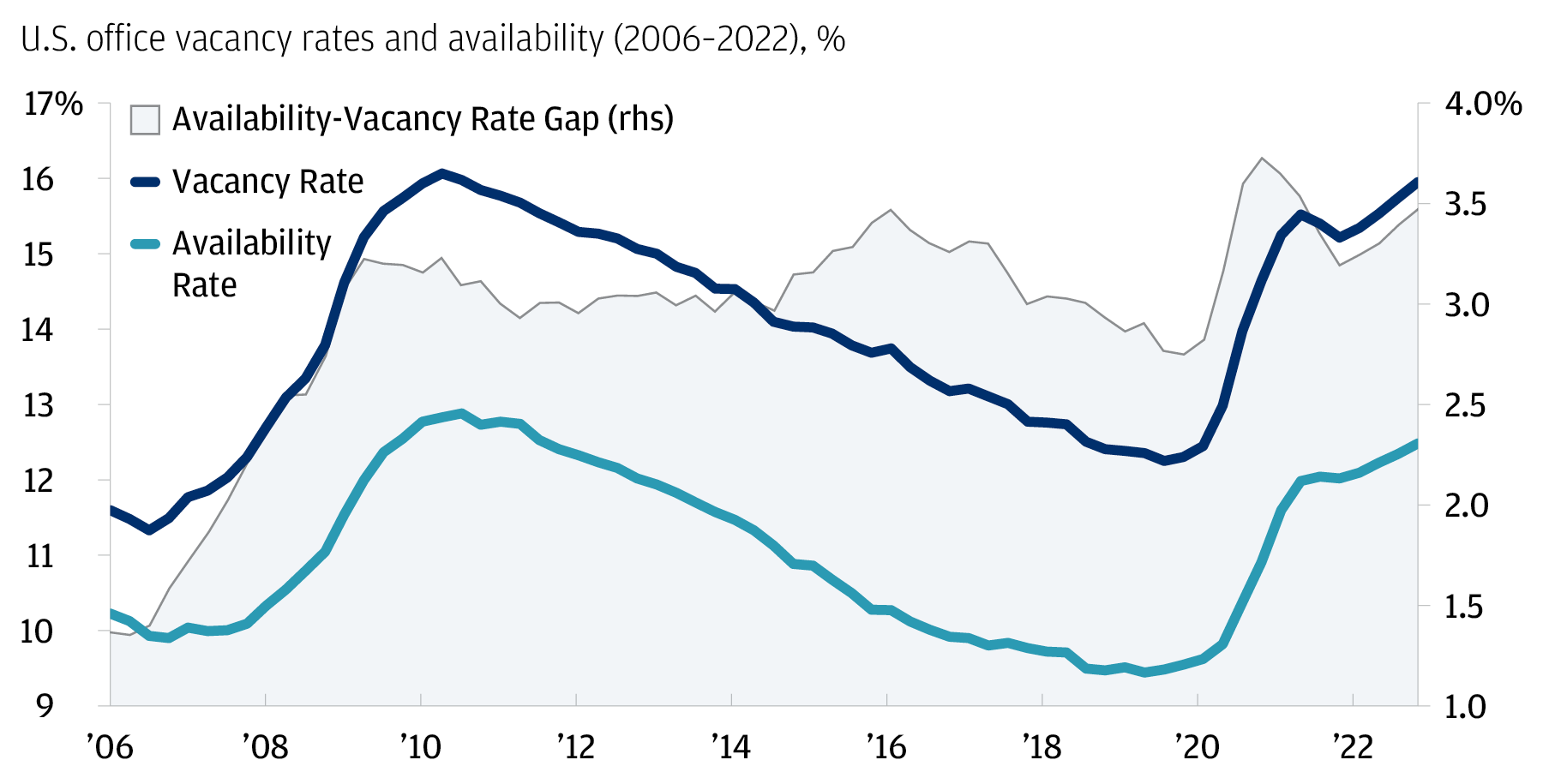

The commercial real estate crisis is unfolding as a significant concern for investors and the broader economy, especially amidst soaring office vacancy rates. With many cities experiencing occupancy levels between 12 percent and 23 percent, the impact on property values has been profound, leading to fears of bank failures and heightened scrutiny of real estate loans. The looming deadlines for a substantial portion of commercial mortgage debt, coupled with persistently high interest rates, pose risks that financial analysts are watching closely. Kenneth Rogoff warns that while the current situation might not trigger a complete meltdown reminiscent of the 2008 financial crisis, it could seriously threaten smaller banks and regional economies. Consequently, understanding how this crisis intertwines with the overall economic landscape is essential for navigating potential fallout in the coming years.

As the landscape of commercial property investing faces a tumultuous chapter, industry experts use terms like “real estate downturn” and “commercial property challenges” to describe the unfolding crisis. The combination of high office vacancy rates and suppressed demand due to evolving work habits has led to significant depreciation in real estate values. Furthermore, these factors are compounded by impending deadlines for a considerable amount of outstanding real estate loans that might turn toxic if economic conditions deteriorate. The fears surrounding potential bank failures are especially acute among smaller institutions heavily invested in commercial properties, which could create ripple effects throughout the financial system. Understanding these dynamics is crucial to anticipating how the ongoing real estate difficulties may affect economic stability on a broader scale.

The Impact of High Office Vacancy Rates on the Economy

High office vacancy rates are emerging as a significant economic concern in the wake of the pandemic, particularly in major urban centers. As businesses adapt to new work models, many are downsizing their office footprints or abandoning traditional spaces altogether. This trend has led to elevated vacancy rates, often ranging between 12% and 23% in cities like Boston, which in turn is resulting in depressed property values. A sustained decrease in demand for office space can trigger a series of economic ramifications, affecting related industries and livelihoods as office buildings become less valuable collateral for lenders, resulting in reduced access to real estate loans.

Furthermore, the declining occupancy rates threaten the financial health of both regional and national banks. With nearly 20% of commercial mortgage debt maturing this year, the likelihood of defaults increases as property owners grapple with lower revenue streams from vacant spaces. This scenario has the potential to destabilize the banking sector, as the pressure mounts for banks with heavy investments in commercial real estate. The cumulative effect of these dynamics might result in a reduction in credit availability, thus constraining consumer spending and slowing overall economic growth.

Understanding the Commercial Real Estate Crisis

The commercial real estate crisis is underscored by significant challenges arising from the convergence of high interest rates and increasing office vacancy rates. The prevailing increase in borrowing costs has made it difficult for many investors to refinance their properties, leading to a high likelihood of defaults as loans come due. The situation is further complicated by the specter of bank failures if these patterns continue unchecked. Kenneth Rogoff highlights that while extensive losses in commercial real estate are imminent, they might not lead to a full-blown financial crisis comparable to the events of 2008-2009.

Despite the dire projections surrounding commercial real estate, it is essential to scrutinize the broader economic landscape. Many institutions, including pension funds and insurance companies, have heavily invested in this sector, and any downturn could result in widespread financial implications. Furthermore, regional banks, which often have more exposure to the real estate market, may face heightened risks as delinquencies rise. If larger banks manage to stabilize through diversified activities and robust regulatory frameworks, it might mitigate the worst of the ripple effects stemming from the commercial real estate crisis.

The Role of Interest Rates in the Real Estate Market

Interest rates play a pivotal role in shaping the trajectory of the real estate market, influencing both borrowing costs and property values. In recent years, historically low rates encouraged a surge in real estate investments, resulting in over-leveraging within the commercial sector. However, as the Federal Reserve has signaled a cautious approach in reducing interest rates, the reality of higher borrowing costs has begun to take its toll. Investors and property owners are now facing the dual challenge of static or declining property values alongside increasing financial obligations, a scenario that is unsustainable in the long term.

For many potential homebuyers and businesses, the rising interest rates could dampen demand, leading to further declines in property prices and exacerbating vacancy rates. This scenario not only threatens the stability of commercial real estate investments but could also embolden financial institutions to tighten lending standards. If lending becomes more restrictive, it may stifle the economic recovery, as businesses struggle to secure resources for operations and expansion, leading to broader implications across sectors reliant on real estate activity.

Regional Banks and the Commercial Real Estate Vulnerability

Regional banks are particularly susceptible to the challenges posed by the commercial real estate market. Many of these institutions have invested heavily in commercial properties that now risk significant devaluation. As observed, the pledge to uphold financial requirements was not uniformly enforced across smaller banks, which may lead them to be more vulnerable as defaults on real estate loans escalate. The potential for regional bank failures could have far-reaching consequences for local economies and communities, especially in areas that rely heavily on these banks for their financial services.

In light of these risks, the Federal Reserve appears to be prepared to step in if necessary, utilizing mechanisms established post-2008 to stabilize the banking sector. However, the impact on consumer access to credit could be profound; lower loan availability can trickle down and affect businesses’ ability to grow, thus impacting hiring and investment. Ultimately, regional banks’ exposure to the commercial real estate crisis embodies a broader narrative of financial exposure that warrants close monitoring as economic conditions continue to evolve.

The Future of Real Estate and Consumer Impact

The ongoing challenges in the commercial real estate sector raise important questions about the future landscape of urban living and its broader economic implications. As vacancy rates soar and office buildings increasingly stand empty, there is a risk of transforming vibrant business districts into ghost towns. For consumers, this could mean a diminished quality of life and less access to amenities. Furthermore, the decline of regional banks due to exposure to commercial real estate could limit credit availability for loans essential for housing, education, and other key areas, thus directly impacting consumer behavior and spending.

Moreover, potential consumers in the market may find themselves at a disadvantage as interest rates continue to rise, further squeezing affordability in an already challenging economic environment. The mismatch between supply and demand in the housing market, combined with rising mortgage costs, could lead to increased housing insecurity for lower and middle-income families. Therefore, mitigating the effects of this crisis may require innovative strategies to repurpose existing spaces and existing financial structures to ensure that consumer needs can still be met despite the prevailing economic landscape.

Strategies to Mitigate the Commercial Real Estate Crisis

Addressing the commercial real estate crisis requires a multifaceted approach that encompasses regulatory, financial, and urban planning strategies. Reassessing zoning laws to allow for adaptive reuse of vacant office buildings might create opportunities for affordable housing solutions without exacerbating existing housing shortages. Additionally, financial institutions should explore innovative refinancing options that could extend the terms of troubled real estate loans, allowing investors breathing room during this transitional period. A proactive stance can help stabilize the market while offering diverse solutions for communities affected by high vacancy rates.

Moreover, collaboration between government entities and financial institutions is crucial in crafting initiatives that support both tenants and property owners. For instance, the implementation of financing programs that incentivize occupancy could encourage businesses to take risks on new office models or co-working spaces. This collaborative approach not only addresses current ecological challenges but revitalizes the commercial landscape in a manner that reflects shifting work dynamics. As trends continue to evolve, ensuring the resilience of the commercial real estate market will be key to fostering economic stability.

Evaluating the Preparedness of Major Banks

The resilience of major banks such as Bank of America, JPMorgan Chase, and Wells Fargo in the face of the commercial real estate crisis is a topic of significant interest. Large banks tend to have diversification strategies that spread risk across different sectors, thereby lessening their vulnerability to downturns in commercial property values. Thus far, their ability to generate high returns from other financial services, alongside strong regulatory oversight, suggests they are better positioned to withstand shocks from commercial real estate defaults compared to their smaller counterparts.

Nevertheless, the dynamics of this crisis remain fluid. As regional banks struggle under the weight of non-performing loans, investor confidence in the banking sector could wane, impacting overall market stability. Additionally, if a major financial institution were to teeter on the brink due to significant exposure in commercial real estate, the ramifications could be profound. It serves as a reminder that while the big banks are in a comparatively stronger position, the interconnectedness of the financial system means that any ripple from the commercial property market can lead to waves in broader market stability.

Consumer Confidence Amidst Economic Uncertainty

In a market characterized by uncertainty, consumer confidence plays a pivotal role in shaping economic outcomes. As high office vacancy rates and rising interest rates weigh heavily on the commercial real estate landscape, consumers may become increasingly cautious in their spending behavior. A climate of financial insecurity can lead to reduced discretionary spending, affecting businesses that rely on consumer patronage and potentially creating a feedback loop that exacerbates economic challenges. The looming potential of widespread bank failures only adds to this anxiety, creating an environment where consumers prioritize stability over engagement.

Yet, it is important to recognize that consumer sentiment is often influenced by overarching economic indicators. In an atmosphere where employment rates remain relatively high, and many investors find themselves benefiting from stock market gains, there may be a counterbalancing effect that sustains spending despite the commercial real estate crisis. This paradox underscores the complex nature of the current economic landscape, suggesting that while immediate pressures may create uncertainty, the broader fundamentals could provide a cushion against deeper economic distress.

Long-Term Outlook for Commercial Real Estate

The outlook for commercial real estate in the long term hinges on various factors, including adjustments to work patterns and evolving consumer preferences. As businesses grapple with the reality of hybrid working models, significant portions of office space may need to be repurposed or redesigned to meet changing demands. This shift toward flexibility may open the door for more creative uses of real estate, spanning from co-working environments to mixed-use developments that incorporate residential and retail spaces. Such evolution can not only alleviate some pressure from high vacancy rates but also breathe new life into stagnant markets.

Additionally, the interplay of interest rates will heavily influence the recovery trajectory of commercial real estate. Should the Federal Reserve adopt a more accommodative monetary policy in response to economic pressures, it could provide the necessary conditions for revitalization within the sector. Conversely, prolonged high interest rates may perpetuate financial strain, leading to further consolidation in the market. The ultimate fate of commercial real estate will depend not only on effective policy responses but also on the ability of stakeholders to innovate and adapt to the challenges posed by a post-pandemic world.

Frequently Asked Questions

What are the implications of high office vacancy rates on the commercial real estate crisis?

High office vacancy rates contribute significantly to the commercial real estate crisis, depressing property values and leading to potential losses for investors. As businesses continue to reduce their office space needs post-pandemic, vacancy rates remain elevated, which could result in a surge of delinquencies on commercial real estate loans.

How do rising interest rates affect the ongoing commercial real estate crisis?

Rising interest rates exacerbate the commercial real estate crisis by increasing borrowing costs for investors, making it challenging to refinance existing loans. This situation may lead to higher rates of default on commercial real estate loans, further destabilizing banks that hold significant amounts of real estate debt in their portfolios.

What role do bank failures play in the commercial real estate crisis?

Bank failures can significantly deepen the commercial real estate crisis by restricting lending and reducing liquidity in the market. As some regional banks struggle with delinquent commercial real estate loans, there is a risk that this could lead to tighter lending conditions for all borrowers, further dampening demand for commercial properties.

What is the impact of the commercial real estate crisis on the economy?

The impact of the commercial real estate crisis on the economy can be substantial, including reduced access to credit, lower consumer spending, and potential job losses in the real estate sector. If regional banks face significant losses, it could lead to a ripple effect that negatively affects other areas of the economy.

Are commercial real estate loans becoming a major risk for banks amid the crisis?

Yes, commercial real estate loans are becoming a major risk for banks as a significant portion of these loans is maturing amid high vacancy rates and reduced demand. Banks that heavily invest in commercial real estate may face substantial losses if defaults increase, particularly among smaller and medium-sized banks less prepared for such risks.

Can the commercial real estate crisis lead to increased interest rates and further economic instability?

The commercial real estate crisis could lead to an increase in interest rates if it results in significant bank failures and a subsequent tightening of credit markets. This would further complicate the economic landscape, making borrowing more expensive during a time when many businesses are struggling to manage high vacancy rates.

What are the long-term solutions to mitigate the commercial real estate crisis?

Long-term solutions to mitigate the commercial real estate crisis involve diversifying investments, improving occupancy rates, and potentially redesigning underutilized office spaces. Additionally, a stable regulatory environment and feasible refinancing options could help alleviate some of the financial pressures on investors and banks.

How are pension funds affected by the commercial real estate crisis?

Pension funds, as major investors in commercial real estate, are directly affected by the crisis. Losses in property values and potential defaults on commercial real estate loans can significantly impact the overall returns of these funds, leading to reduced benefits for retirees and financial strain for pension systems.

| Key Points | Details |

|---|---|

| High Office Vacancy Rates | Office vacancy rates are between 12% to 23% post-pandemic, affecting property values. |

| Surge in Real Estate Loans | 20% of $4.7 trillion in commercial mortgage debt is due this year, potentially impacting banks. |

| Concerns about Bank Failures | While some banks may face issues, a full-blown financial crisis is not anticipated like in 2008. |

| Impact on Economy | Losses in commercial real estate could affect regional banks and consumption patterns. |

| Regional Bank Vulnerability | Smaller banks are at risk due to lesser capital requirements and exposure to commercial real estate. |

| Big Banks Resilience | The largest banks are more diversified and in better positions to handle the ongoing challenges. |

Summary

The commercial real estate crisis presents significant challenges in 2024, with high office vacancy rates and an impending surge of real estate loans coming due. Kenneth Rogoff suggests that while this situation could result in significant losses for some investors and regional banks, it is unlikely to lead to a financial meltdown similar to that of 2008. The dynamics of the current market, characterized by a solid job market and booming stock market, indicate that the overall economy remains resilient, despite the pockets of distress in the commercial real estate sector.